Investors are racing to work out how much monetary policy tightening the economy can handle as the U.S. Federal Reserve embarks on its rate-hike cycle, with some expecting an even steeper path ahead as others fret over possible missteps.

The Fed’s first rate hike since 2018 on Wednesday was baked into markets, but the central bank surprised by projecting the equivalent of a quarter-percentage-point rate increase at each of its six remaining policy meetings this year.

Hiking rates should tame sky-high inflation that is biting at people’s ability to purchase everyday items, but it runs the risk of crimping growth and tipping the economy into recession. Still, Fed Chair Jerome Powell expressed confidence the economy could flourish despite less accommodative policy. read more

“The Fed (is) trying to right the ship,” said Andy Kapyrin, chief investment officer of RegentAtlantic. “My expectation is that they will get more hawkish as the year goes on, especially if inflation stays high.”

Kapyrin is increasing overweights in value stocks – shares of comparatively cheap, economically sensitive companies that tend to thrive in an environment of strong growth and higher rates – as well as floating rate bonds he expects to benefit from rising borrowing costs.

The speed at which the Fed is moving drew some comparisons to former Fed chairman Paul Volcker, who sharply raised rates in 1979 in a fight to tame double digit inflation, with analysts at research firm Bespoke saying Powell was having a “mini Volcker moment.”

Still, the clarity on the Fed’s projected rate hike path and the central bank’s insistence that the economy is strong enough to handle a cocktail of policy tightening, higher inflation and volatile commodity prices in the wake of Russia’s invasion of Ukraine, reassured some.

“The big overhang for the market was the uncertainty as to what the Fed was going to do, and now we have a rate path,” said Jay Hatfield, portfolio manager at Infrastructure Capital Advisors.

The benchmark S&P 500 closed up more than 2%, a move that some investors took as relief that the Fed has kicked off its inflation fight. read more

The pace of rate hikes and balance sheet tightening could, however, weigh on the economy. Powell said details on reducing the Fed’s nearly $9 trillion balance sheet could be finalized in May. read more

“It is good that the Fed left sort of unclear when they will start reducing their balance sheet,” said Troy Gayeski, Chief Market Strategist at FS Investments. “We have real concerns over whether the markets can continue to function if the Fed starts to drain their balance sheet more aggressively.”

EYES ON RISK

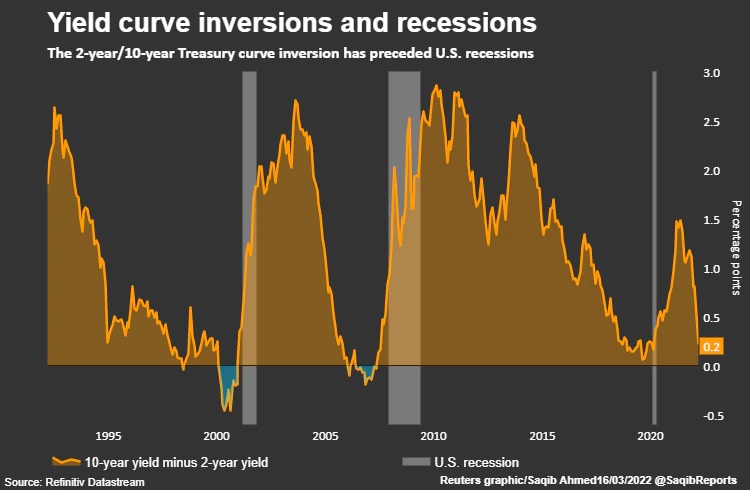

Some concerns over future growth were apparent in the Treasury market, with yields on some shorter-dated Treasuries rising above longer-dated ones, a sign that investors see economic risks ahead.

The yield curve between two-year and 10-year notes flattened, the yield gap between five-year notes and 30-year bonds shrank to the smallest since October 2018 and yields on five-year notes rose above those on 10-year notes, showing an inversion for the first time since March 2020 .

An inverted yield curve has been a reliable predictor of past economic downturns in key parts of the curve, although the closely-watched parts of the curve most associated with recession have not yet flipped.

The 2-year/10-year Treasury curve inversion has preceded U.S. recessions

“The longer that curve stays flat or begins to flatten, or if it does start to invert throughout the curve, that would be a concern of ours,” said Joe Bell, chief investment officer at Meeder Investment Management.

Fed policymakers began to discount the new risks facing the global economy, marking down their gross domestic product growth estimate for 2022 to 2.8%, from the 4% projected in December.

“They don’t have a great record in engineering ‘soft landings’,” said Matthew Nest, global head of active fixed income at State Street Global Advisors, who expects the economy to shrink in the first half of 2023.

There could however be relief if commodity prices ease, said Tony Rodriguez, head of fixed income strategy at asset manager Nuveen, who is moving into low quality mortgage bonds and high yield corporate bonds. That could take pressure off the Fed to tighten rates as much as it has projected, he said.

“If we have learned anything over the past two years it’s that the Fed’s economic projections are more often than not a little bit off base,” he said.

Photo credit to: Reuters

News source: Reuters